Get 69% Off on Cloud Hosting : Claim Your Offer Now!

- Products

- Solutions

-

Solutions

-

Cloud

Hosting

Cloud

Hosting

-

VPS

Hosting

-

GPU

Cloud

GPU

Cloud

-

Dedicated

Server

Dedicated

Server

-

Server

Colocation

Server

Colocation

-

Backup as a Service

Backup as a Service

-

CDN

Network

CDN

Network

-

Window

Cloud Hosting

Window

Cloud Hosting

-

Linux

Cloud Hosting

Linux

Cloud Hosting

-

Managed

Cloud Service

-

Storage

as a Service

Storage

as a Service

-

VMware

Public Cloud

-

Multi-Cloud

Hosting

-

Cloud

Server Hosting

-

Bare

Metal Server

-

Virtual

Machine

-

Magento

Hosting

Magento

Hosting

-

Remote

Backup

Remote

Backup

-

DevOps

DevOps

-

Kubernetes

Kubernetes

-

Cloud

Storage

Cloud

Storage

-

NVMe

Hosting

NVMe

Hosting

-

DR

as s Service

DR

as s Service

-

-

Solutions

- Marketplace

- Pricing

- Resources

- Company

Pricing

Calculator

Pricing

Calculator

Power

Power

Utilities

Utilities VMware

Private Cloud

VMware

Private Cloud VMware

on AWS

VMware

on AWS VMware

on Azure

VMware

on Azure Service

Level Agreement

Service

Level Agreement Table of Contents

- Introduction: The Evolution of Germany’s Colocation Landscape

- What Are Colocation Providers?

- Understanding Germany’s Colocation Market Dominance

- Top Colocation Providers in Germany: Comprehensive Overview

- Regional Distribution and Market Opportunities

- Technology Trends Reshaping German Colocation

- Industry-Specific Colocation Solutions

- Pricing Models and Cost Considerations

- Future Outlook: What’s Next for Germany’s Colocation Market

- Elevate Your Infrastructure with Germany’s Premier Colocation Solutions

- Frequently Asked Questions (FAQs)

- 1. What makes Germany an attractive location for colocation services?

- 2. How do colocation costs in Frankfurt compare to other German cities?

- 3. What power density should I plan for in modern colocation deployments?

- 4. How important is Tier certification when choosing a colocation provider?

- 5. What is the typical contract length for colocation services in Germany?

- 6. How does colocation compare to building a private data center?

- 7. What connectivity options should I expect from top colocation providers?

- 8. How do German data protection laws affect colocation decisions?

- 9. What is the role of sustainability in modern colocation selection?

Introduction: The Evolution of Germany’s Colocation Landscape

Are you searching for top colocation providers in Germany to power your enterprise infrastructure?

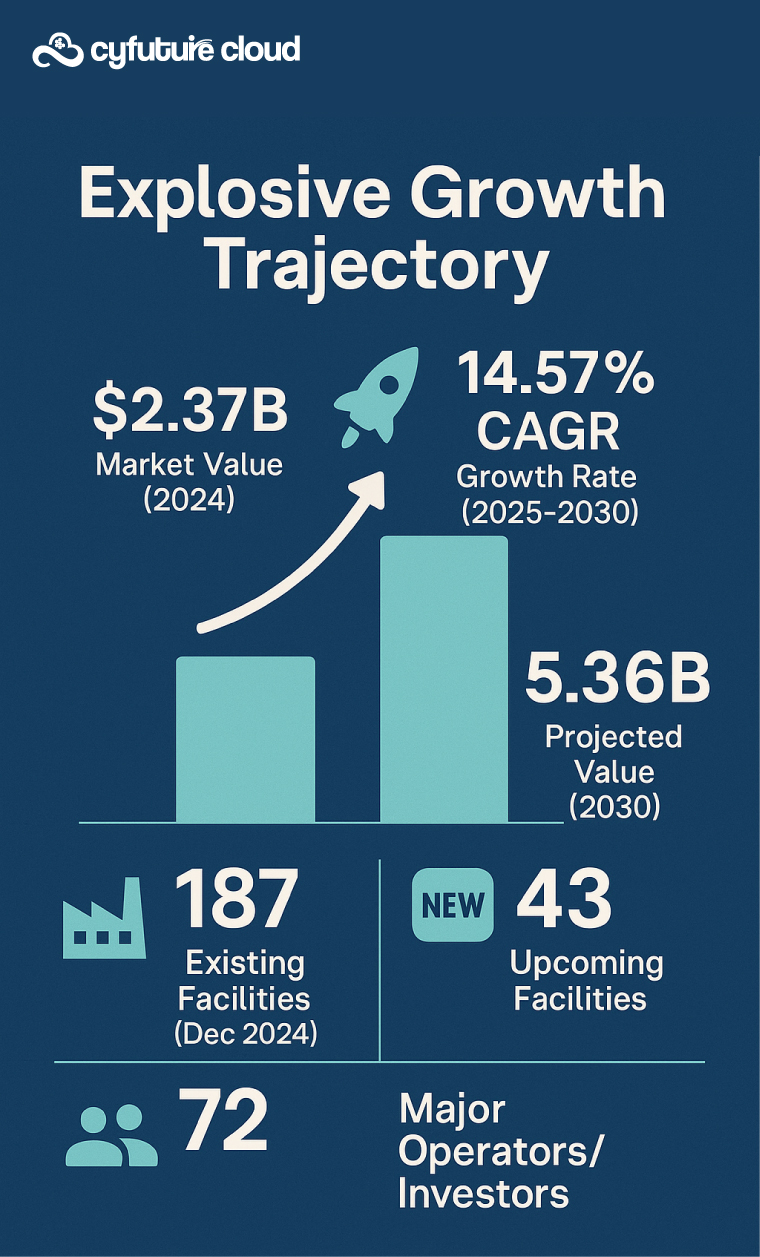

Germany has emerged as Europe’s most dynamic data center hub, with the colocation market valued at USD 2.37 billion in 2024 and projected to reach USD 5.36 billion by 2030, reflecting a robust CAGR of 14.57%. With 187 existing colocation facilities and Frankfurt commanding 59.92% of market share, Germany offers unparalleled opportunities for enterprises seeking world-class infrastructure.

The German colocation landscape is experiencing unprecedented transformation. Here’s why:

With over 187 operational colocation data centers as of December 2024, Germany stands as one of Europe’s four leading markets alongside the United Kingdom, Netherlands, and France. Frankfurt alone hosts more than 72 operational facilities, establishing itself as the undisputed leader in continental Europe’s data center operations.

What Are Colocation Providers?

Colocation providers are specialized data center operators that offer businesses the ability to house their IT infrastructure—servers, storage systems, and networking equipment—in professionally managed facilities. Instead of building and maintaining expensive on-premise data centers, organizations can leverage shared infrastructure while maintaining complete control over their hardware and software.

Think of it this way:

A colocation facility operates like a high-security apartment building for servers, where businesses rent space and share utilities while retaining ownership and management of their equipment. This model delivers enterprise-grade power, cooling, connectivity, and security without the massive capital expenditure required for proprietary facilities.

Understanding Germany’s Colocation Market Dominance

Market Dynamics and Growth Trajectory

The German data center market has reached a valuation of USD 7.71 billion in 2024 and is projected to soar to USD 12.84 billion by 2030—representing an impressive annual growth rate of 8.87%. The colocation sector specifically commanded 81.70% of market share in 2024, underscoring its critical role in Germany’s digital infrastructure.

Let’s break down the numbers:

Power Capacity Expansion: Germany’s upcoming power capacity is projected to reach 3 GW, effectively doubling the current 1.5 GW. Over 1,760 MW of power capacity will be added across Germany during 2025-2030, reflecting the massive infrastructure investments underway.

Facility Growth: With 43 upcoming facilities joining the existing 187 operational centers, the upcoming rack capacity is expected to exceed 350,000 racks. Frankfurt’s operational capacity alone stands at 745 MW of live IT load, with 542 MW under construction and another 383 MW in planning stages.

AI-Driven Demand: Microsoft’s EUR 3.2 billion investment program aims to double Germany’s national AI capacity by 2026, while Deutsche Telekom targets 10,000 edge nodes by 2030 to support 5G low-latency use cases.

Why Frankfurt Dominates European Colocation

Frankfurt has earned its position as Europe’s second-largest data center market after London for compelling reasons:

Strategic Connectivity: Home to DE-CIX, where approximately 1,000 international networks interconnect, Frankfurt offers unmatched carrier density and sub-millisecond reach to European finance hubs. This connectivity ecosystem is irreplaceable for organizations requiring low-latency cross-connects.

Financial Hub Proximity: The city’s robust financial services industry creates consistent demand for high-performance, ultra-secure colocation services. Banking, financial services, and insurance workloads are projected to advance at 13.18% CAGR through 2030.

Geographic Advantage: Frankfurt’s central European location provides optimal access to major markets across the continent, making it ideal for businesses requiring pan-European reach.

Top Colocation Providers in Germany: Comprehensive Overview

1. Cyfuture Cloud – Rising Star in German Colocation

Cyfuture Cloud has established itself among the premiere top colocation providers in Germany, bringing over two decades of expertise to the European market. The company offers:

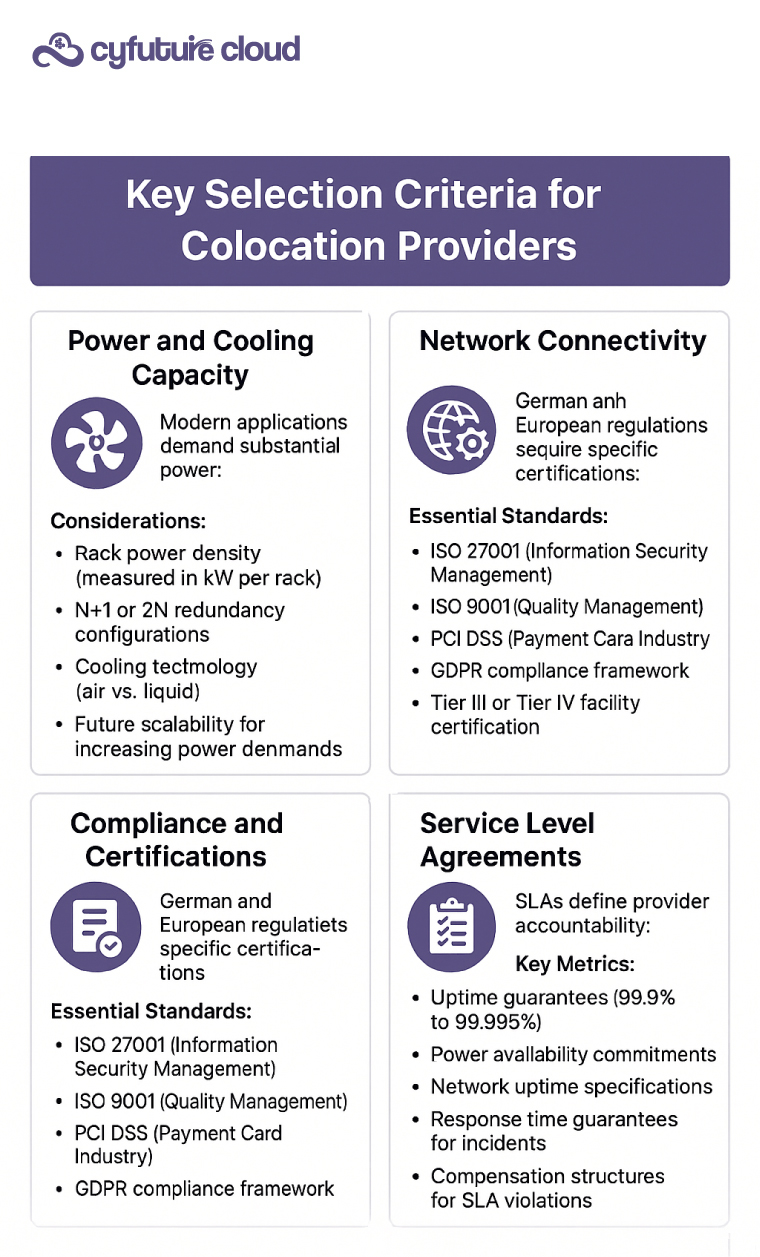

Tier III Certified Infrastructure: Cyfuture Cloud’s data centers meet rigorous Tier III certification standards, ensuring 99.982% uptime guarantee with redundant power, cooling, and network pathways.

Comprehensive Security: Multi-layered physical security featuring biometric access control, 24/7 CCTV surveillance, mantraps, and on-site security personnel. All facilities comply with ISO 27001 and PCI DSS standards.

Flexible Scalability: From single rack units to full cage deployments, Cyfuture Cloud provides customizable solutions that grow with your business needs. Their high-density infrastructure supports rack loads of 2 tons with earthquake-resistant RCC framing.

Competitive Advantage: Cyfuture Cloud’s client-centric approach has earned them six-year relationships with enterprises seeking improved network security, redundant power supply, and elimination of telecom fraud challenges.

2. NTT DATA – Germany’s Largest Operator

NTT DATA holds the distinction of being Germany’s largest data center operator by IT power capacity. With revenues growing from USD 1.25 billion in 2020 to USD 1.80 billion in 2024 (CAGR of 9.7%), NTT demonstrates consistent market leadership.

Global Footprint: Operating over 160 data centers across 20+ countries with 600,000 square meters of space and 2,100 MW of critical IT load, NTT brings unmatched global scale to German operations.

Service Portfolio: Offers custom cages, turnkey cabinet solutions, private suites, powered shells, and build-to-suit designs tailored to enterprise requirements.

Upcoming Developments: Leading the charge in new capacity additions through large-scale developments, particularly in Frankfurt and emerging markets like Berlin.

3. Digital Realty – Hyperscale Excellence

Digital Realty exhibits remarkable revenue momentum, growing from USD 3.90 billion in 2020 to approximately USD 5.55 billion in 2024. As one of the top colocation providers in Germany, Digital Realty excels in hyperscale deployments.

PlatformDIGITAL Ecosystem: Supports data gravity and hybrid cloud strategies critical for modern enterprise demands, enabling seamless integration between on-premise and cloud infrastructure.

Sustainability Focus: Commitment to sustainable infrastructure positions Digital Realty as a leader in environmentally responsible data center operations—crucial given Germany’s strict environmental regulations.

Strategic Partnerships: The company’s collaboration with CoreWeave to deploy AI-ready high-density GPU colocation demonstrates its forward-thinking approach to emerging technologies.

4. Equinix – Global Interconnection Leader

Equinix operates 260+ data centers across 33 countries, making it the world’s most globally pervasive colocation provider. In Germany, Equinix’s interconnection-dense IBX (International Business Exchange) facilities set industry standards.

Platform Equinix: Creates a digital ecosystem where thousands of companies interconnect, enabling network effects that reduce latency and improve application performance.

xScale Program: Originally a retail-focused provider, Equinix’s xScale initiative now serves hyperscale clients, demonstrating market adaptability.

Recent Expansion: Continued investments in Frankfurt and emerging German markets underscore Equinix’s commitment to maintaining leadership among top colocation providers in Germany.

5. CyrusOne – Rapid International Expansion

With 50+ data centers spanning multiple continents, CyrusOne represents the new wave of globally ambitious colocation providers. The company is leveraging private equity backing to aggressively expand outside its home market.

European Strategy: Significant investments in Germany position CyrusOne to compete head-on with established leaders like Equinix and Digital Realty.

High-Density Capabilities: Specialized infrastructure supporting modern workloads, including AI and machine learning applications requiring substantial power density.

Additional Major Players

AtlasEdge: Expanding edge computing capabilities across German markets.

Colt Data Centre Services: Carrier-focused solutions with extensive network connectivity.

Global Switch: Large-scale campus facilities optimized for hyperscale deployments.

Iron Mountain: Combining colocation with comprehensive data management services.

Vantage Data Centers: Recent launches of three new facilities (two in Berlin, one in Frankfurt) demonstrate aggressive expansion strategy.

Maincubes: German energy expertise applied to data center operations.

VIRTUS Data Centres: Leading upcoming supply through innovative developments.

Regional Distribution and Market Opportunities

Frankfurt: The Established Powerhouse

Frankfurt’s dominance extends beyond raw numbers. The city offers:

- Mature Ecosystem: Over 72 operational facilities create a dense interconnection fabric

- DE-CIX Access: Direct connectivity to one of the world’s largest internet exchange points

- Financial Services Focus: Specialized infrastructure meeting stringent regulatory requirements

- Challenge: Land prices exceeding EUR 4,500 per square meter and grid queues exceeding two years

Berlin-Brandenburg: The Rising Challenger

Berlin-Brandenburg has become Germany’s second-largest data center location, with capacity tripling between 2017 and 2023. The region is projected to experience fivefold capacity increases in coming years.

Advantages:

- Lower real estate costs compared to Frankfurt

- Growing tech ecosystem attracting cloud-native companies

- Government digitization initiatives creating demand

- Strategic location for Eastern European connectivity

Munich: The Innovation Hub

Munich’s strong manufacturing and technology sectors create unique colocation opportunities, particularly for:

- Industrial IoT applications

- Automotive industry cloud deployments

- Research and development infrastructure

- Media and entertainment rendering workloads

Emerging Markets

Secondary cities including Hamburg, Cologne, Dresden, and Stuttgart offer:

- Cost advantages over primary markets

- Regional redundancy options

- Proximity to specific industry clusters

- Less congested network infrastructure

Technology Trends Reshaping German Colocation

Artificial Intelligence Infrastructure

AI is fundamentally transforming data center requirements. Here’s what’s changing:

Power Density Requirements: AI racks now draw 30-100 kW, a fivefold increase from traditional enterprise footprints. Average hyperscale utilization in Frankfurt exceeds 85%, tightening available supply.

Cooling Innovation: Liquid cooling systems, particularly Single-Phase Direct Liquid Cooling, enable efficient heat dissipation for high-density GPU deployments. By 2025, up to 85% of newly delivered Nvidia chips are expected to be designed for liquid cooling.

Market Opportunity: The generative AI segment is projected to grow 560% by 2031, reaching USD 16.5 billion—creating massive demand for specialized colocation infrastructure.

Edge Computing Revolution

Deutsche Telekom’s ambitious plan to deploy 10,000 edge nodes by 2030 exemplifies the edge computing revolution. Edge sites, while smaller, are projected for 13.3% CAGR as 5G adoption accelerates localized processing requirements.

Business Impact:

- Reduced latency for real-time applications

- Enhanced user experiences for mobile services

- Support for autonomous vehicles and IoT deployments

- Distributed computing architectures

Sustainability and Environmental Compliance

Germany’s commitment to environmental responsibility shapes colocation operations:

Renewable Energy: 88% of electricity consumed in German colocation data centers already comes from renewable sources. Furthermore, 69% of operators have concluded Power Purchase Agreements (PPAs) for long-term renewable energy coverage.

Waste Heat Utilization: The Energy Efficiency Ordinance (EnEfG) increasingly mandates waste heat utilization. Data centers are being integrated into urban heating networks, creating circular economy opportunities.

PUE Performance: German data centers achieve PUE scores ranging from 1.12 to 1.50, with an average of 1.29—demonstrating exceptional energy efficiency.

Hybrid and Multi-Cloud Integration

The top colocation providers in Germany are enhancing cloud connectivity services:

Direct Connect Services: Providers offer direct connections to major cloud platforms (AWS, Microsoft Azure, Google Cloud) reducing latency and improving security.

Hybrid IT Support: Colocation enables businesses to combine on-premise systems with cloud-based solutions, maintaining control over sensitive data while leveraging cloud scalability.

Network Fabric Evolution: Software-Defined Networking (SDN) enables more flexible and efficient network management in colocation environments.

Industry-Specific Colocation Solutions

Financial Services

Banking, financial services, and insurance sectors drive 55.74% of market demand, with workloads advancing at 13.18% CAGR through 2030:

- Ultra-low latency trading infrastructure

- Regulatory compliance and data sovereignty

- High-frequency trading connectivity

- Disaster recovery and business continuity

Manufacturing and Industry 4.0

Germany’s manufacturing excellence creates unique requirements:

- Industrial IoT edge processing

- Factory floor connectivity

- Supply chain optimization systems

- Predictive maintenance platforms

Media and Entertainment

Content creation and distribution needs:

- High-bandwidth video rendering

- Content delivery network points of presence

- Post-production processing

- Real-time streaming infrastructure

Healthcare and Life Sciences

Data-intensive medical applications:

- Medical imaging processing

- Genomic research computing

- Telemedicine infrastructure

- Patient data management systems

Pricing Models and Cost Considerations

Understanding colocation pricing requires evaluating multiple components:

Space-Based Pricing

- Per Rack Unit (U): Charged per 1.75-inch increment

- Half or Full Rack: Fixed monthly rates for cabinet space

- Cage Enclosures: Private areas for multiple racks

- Suite Deployments: Dedicated rooms for large deployments

Power Pricing

- Flat Rate: Fixed monthly power allocation (e.g., 1kW per cabinet)

- Metered Billing: Pay for actual usage in kWh

- Circuit-Based: Charged by circuit capacity regardless of usage

- High-Density Premiums: Additional charges for power-intensive workloads

Network and Bandwidth

- Included Allocation: Monthly bandwidth allowance (e.g., 10TB, 100TB)

- Overage Charges: Fees for exceeding included bandwidth

- Committed Information Rate: Guaranteed minimum bandwidth

- Unmetered Options: Unlimited bandwidth at fixed cost

Location Premium

Data centers in Frankfurt typically command 15-30% higher pricing than secondary markets due to:

- Prime real estate costs

- Dense interconnection ecosystems

- Financial services infrastructure

- Limited available capacity

Future Outlook: What’s Next for Germany’s Colocation Market

Market Growth Projections

Multiple scenarios paint a robust growth picture:

Conservative Estimate: USD 3.55 billion by 2029 (8.37% CAGR) Moderate Projection: USD 5.36 billion by 2030 (14.57% CAGR) Optimistic Forecast: USD 7.34 billion by 2030 (15.8% CAGR)

Capacity Expansion

Physical Infrastructure:

- 350,000+ new rack capacity

- 3 GW total power capacity (doubling current levels)

- 43 new facilities joining existing footprint

- Expansion into secondary markets

Technology Evolution

Next-Generation Infrastructure:

- Quantum computing readiness

- 5G and eventual 6G edge nodes

- Advanced liquid cooling systems

- AI-optimized facility designs

Regulatory Landscape

Emerging Requirements:

- Mandatory waste heat utilization

- Stricter renewable energy mandates

- Enhanced cybersecurity standards

- Data sovereignty requirements

Investment Climate

Over EUR 24 billion in investments are projected for German data center infrastructure through 2029, driven by:

- Hyperscale cloud expansion (Amazon, Microsoft, Google)

- Retail sector digitization (Schwarz Group/Lidl investments)

- Financial services modernization

- Government digitization initiatives

Elevate Your Infrastructure with Germany’s Premier Colocation Solutions

Germany’s colocation market is booming—projected to reach USD 5.36 billion by 2030 with 6,230 MW of IT capacity. The top colocation providers in Germany are investing billions to meet explosive demand.

From Cyfuture Cloud’s client-centric approach to Equinix’s dense interconnection and Digital Realty’s hyperscale expertise, Germany delivers world-class infrastructure for every enterprise need.

Ready to transform your infrastructure strategy?

Partner with leading top colocation providers in Germany to unlock enterprise-grade power, connectivity, and security. With 187 facilities operational and 43 more launching soon, now is the time to act.

Leverage premium colocation solutions to reduce costs, boost performance, and accelerate digital transformation. The future combines cloud flexibility with colocation’s control—delivering the best of both worlds.

Frequently Asked Questions (FAQs)

1. What makes Germany an attractive location for colocation services?

Germany offers strategic advantages including its position as Europe’s largest economy, stringent data protection laws (GDPR compliance), excellent connectivity infrastructure (especially through DE-CIX in Frankfurt), and growing demand from financial services, manufacturing, and cloud sectors. The market is projected to grow from USD 2.37 billion (2024) to USD 5.36 billion (2030).

2. How do colocation costs in Frankfurt compare to other German cities?

Frankfurt typically commands 15-30% higher pricing than secondary markets like Berlin, Munich, or Hamburg. This premium reflects Frankfurt’s dense interconnection ecosystem, proximity to financial hubs, and limited available capacity. However, Frankfurt’s connectivity advantages often justify the higher costs for latency-sensitive applications.

3. What power density should I plan for in modern colocation deployments?

Traditional enterprise racks typically require 2-5 kW per rack. However, AI and GPU-intensive workloads now demand 30-100 kW per rack. When selecting a colocation provider, ensure they can support your current requirements plus 50-100% growth capacity for future needs. High-density deployments often require liquid cooling solutions.

4. How important is Tier certification when choosing a colocation provider?

Tier certification (Tier I-IV) indicates facility redundancy and uptime capability. Tier III facilities (99.982% uptime) offer N+1 redundancy and concurrent maintainability—suitable for most enterprises. Tier IV (99.995% uptime) provides 2N redundancy for mission-critical applications. However, operational excellence matters more than certification alone; evaluate provider track record and SLAs.

5. What is the typical contract length for colocation services in Germany?

Standard contracts range from 12 to 36 months for retail colocation (single racks or cabinets). Wholesale deployments (cage or suite-level) typically require 3-5 year commitments. Longer terms often secure better pricing but reduce flexibility. Some providers now offer month-to-month options at premium rates.

6. How does colocation compare to building a private data center?

Private data centers require massive capital expenditure (often EUR 10-50 million minimum), ongoing operational costs, and dedicated staff. Colocation eliminates upfront infrastructure investment, reduces operational complexity, and provides enterprise-grade facilities for monthly operational expenses. For most organizations, colocation offers superior economics and faster deployment.

7. What connectivity options should I expect from top colocation providers?

Leading providers offer carrier-neutral facilities with access to 10+ telecommunications carriers, direct connections to major internet exchanges (especially DE-CIX), cloud on-ramps to AWS/Azure/Google Cloud, and diverse fiber paths for redundancy. Expect bandwidth options from 1 Gbps to 100+ Gbps with both metered and unmetered pricing models.

8. How do German data protection laws affect colocation decisions?

Germany’s strict interpretation of GDPR and data sovereignty requirements often mandate that personal data of German/EU residents remain within EU borders. This regulatory environment makes German colocation attractive for organizations requiring compliance. Top providers offer comprehensive compliance support including ISO 27001, PCI DSS, and GDPR frameworks.

9. What is the role of sustainability in modern colocation selection?

With 88% of German colocation electricity already from renewable sources and mandatory waste heat utilization coming soon, sustainability is increasingly critical. Evaluate providers’ PUE scores (target 1.3 or below), renewable energy commitments, and waste heat recovery programs. Sustainable operations also reduce long-term energy costs and regulatory risk.

Recent Post

Stay Ahead of the Curve.

Join the Cloud Movement, today!

Send this to a friend